Reality Check: Structural Slowdown or Temporary Pause

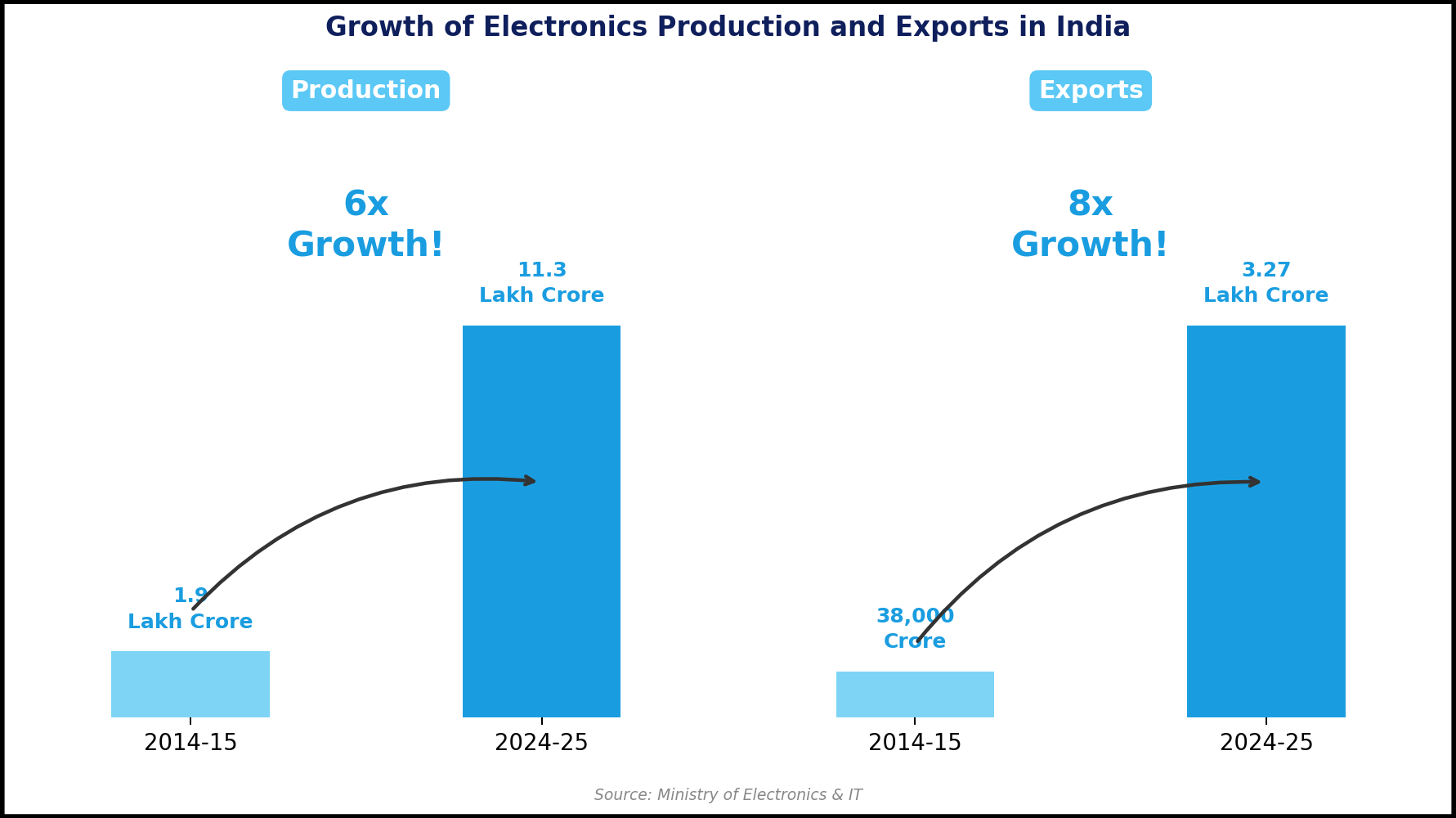

India’s Electronic Manufacturing Services (EMS) sector has seen a remarkable transformation in the post-COVID years, emerging as one of the strongest drivers of wealth creation in India’s domestic market. The broader electronics industry has expanded nearly 6x over the last decade, growing from around ₹1.9 lakh crore in FY15 to ₹11.3 lakh crore in FY25. Many players have grown multiplefold - Amber Enterprises for instance, has scaled from roughly ₹1,000 Cr in annual revenue a decade ago to nearly ₹11,800 Cr today. Where as Dixon Tech went from ₹1,300 Cr to over ₹48,000 Cr in FY2026 (36 times in a decade!).

This phase of hyper growth has also followed massive wealth creation that has taken place over last 5 to 7 years. Overall, the listed Indian EMS players collectively created ₹1-1.5 lakh crore of equity wealth for investors post covid.

But after a massive rally in both earnings & stock prices over the last few years, the sector appears to be entering a tougher phase. Recent quarterly results from several leading players suggest that growth is becoming harder to sustain, with companies now facing a mix of operational challenges and industry-wide headwinds.

Some of the early Production-Linked Incentive (PLI) schemes, including the mobile manufacturing PLI ending in 2026, are nearing expiry. As government incentives gradually reduce, the cost advantages that helped early EMS players scale rapidly may start fading and markets seems to have already pricing for sharper competition and lower profitability across the sector.

Another key issue has been rising working capital pressure. Although most EMS contracts allow companies to pass on higher raw material costs to customers, the process is rarely immediate. For many Tier-2 suppliers (who don’t directly manfacture for brands), there is also a typically lag of one or two quarters before these costs can be fully recovered. In a volatile supply chain environment, this delay has led to longer working capital cycle, starting to weigh on margins and cash flows.

At the same time, not all problems are industry-wide. A few challenges are specific to the segments in which these EMS companies operate. Consumer electronics, appliances, telecom, and export-focused businesses are all seeing different demand trends and inventory cycles. In this write-up, we discuss the issues emerging across key EMS players and evaluate whether the broader India manufacturing thesis still holds strong.

Dixon Tech - Flag Bearer of Electronics Manufacturing

While Dixon’s revenues have grown nearly 36x over the last decade, the company’s business model today remains heavily tied to the global smartphone cycle. Nearly 72% of its revenue comes from the mobile manufacturing segment, making its performance closely linked to the health of the smartphone industry.

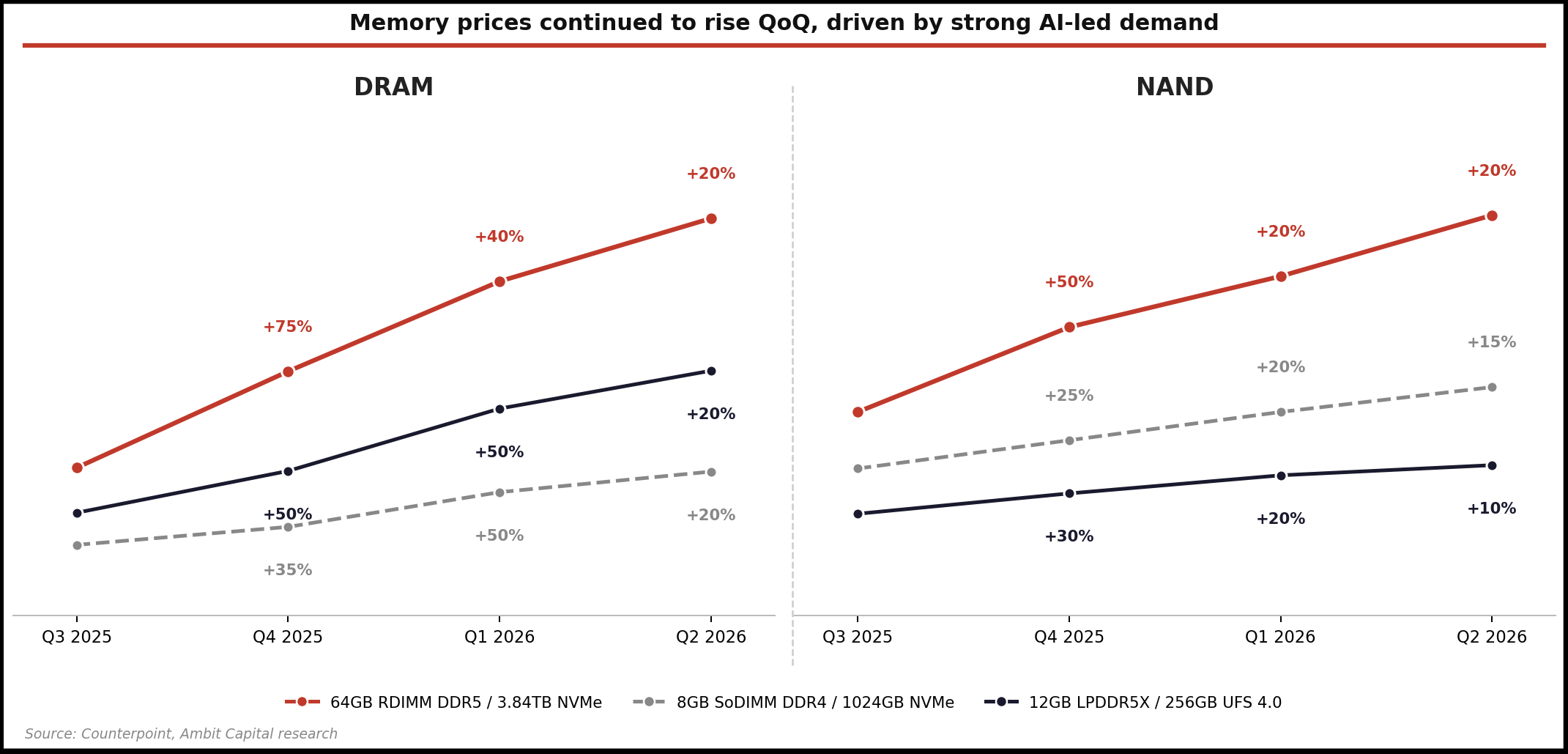

Over the last few quarters, the smartphone ecosystem has started facing multiple pressures simultaneously. An AI-led surge in demand for high-end computing infrastructure has created an unprecedented shortage of memory chips and RAM globally, pushing component prices sharply higher. While premium brands like Apple and Samsung Electronics have been able to pass on these costs through price hikes, the stress is far more visible in the affordable and mid-tier smartphone categories, especially in the sub-₹15,000 segment where pricing power is limited.

This matters because a large share of India’s smartphone volumes still comes from value-focused consumers. Rising component costs, a weaker INR, and broader macro pressures are already hurting demand in these categories. Even though EMS companies like Dixon largely operate on cost pass-through arrangements and remain relatively protected at a gross margin level, they are not insulated from slower volumes. Lower shipments directly impact operating leverage, especially in a scale-driven business.

Globally too, smartphone demand has started weakening. Shipments declined around 6% YoY in 1QCY26, and industry expectations suggest 2026 could see a much sharper downturn. After growing 3% in 2025, global smartphone shipments are now expected to decline by nearly 12% in 2026, potentially falling below 1.1 billion units for the first time since 2013. Most smartphone brands, except Apple, have already reported volume declines in early 2026.

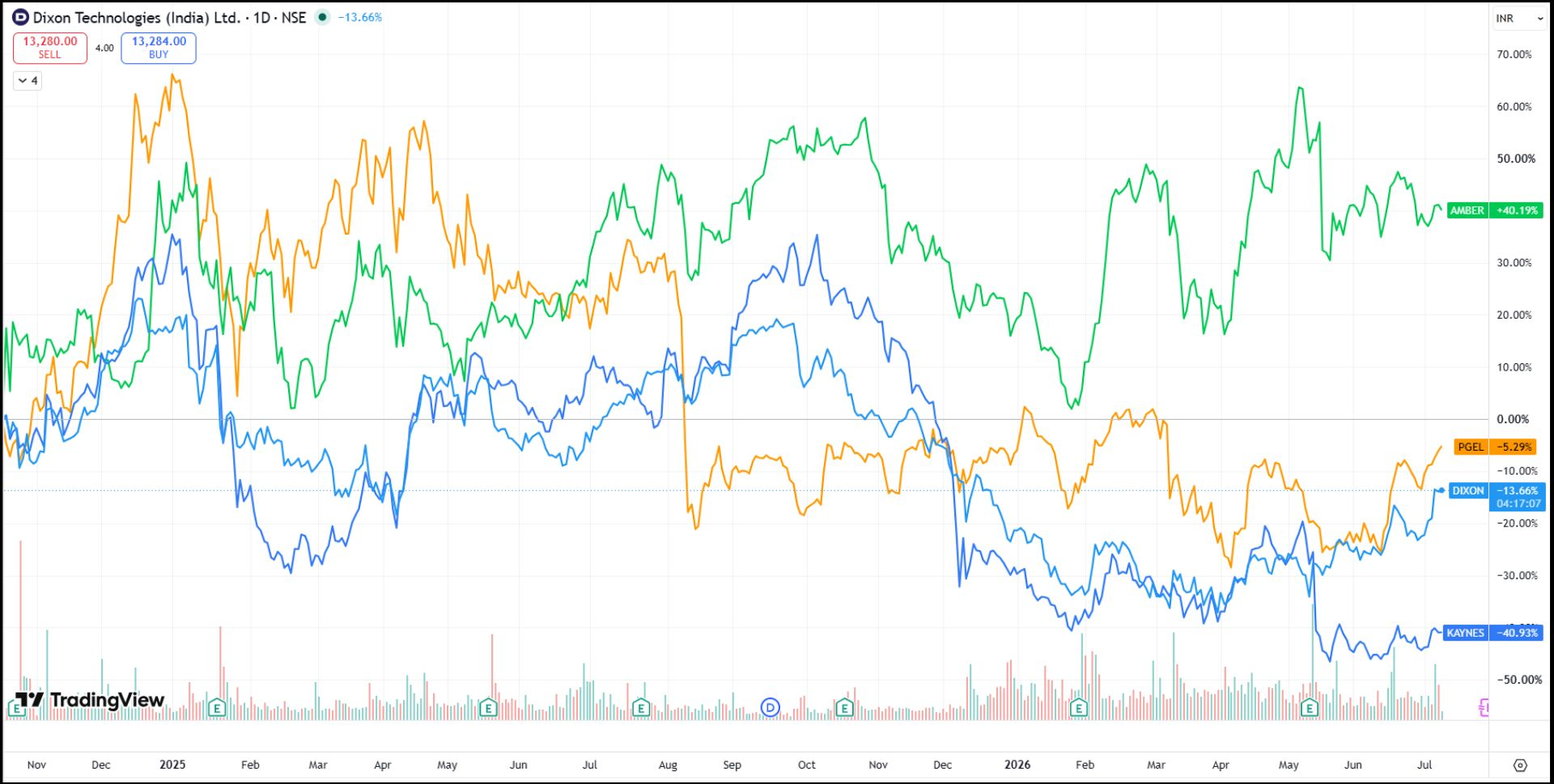

This backdrop partly explains why Dixon’s stock has corrected nearly 40% from its peak. Apart from broader industry weakness, the company has also faced certain client-specific challenges too, that have added to investor concerns.

Kaynes Tech – When Working Capital Becomes the Risk

While Kaynes Tech emerged as one of the biggest beneficiaries of India’s EMS boom, investor concerns have recently started shifting from growth to the quality of that growth. Unlike Dixon, where product concentration has become a key issue, Kaynes is facing significant stress because of customer and segment exposure, particularly within smart metering.

The smart metering business once contributed the majority of revenues but now accounts for around 24% of FY26 revenue. However, despite the falling revenue contribution, the segment still accounts for nearly 89% of total receivables, which increased sharply by almost 3x during FY26. Delays in rural meter installations, along with slower payment cycles in government-linked projects, ended up stretching the balance sheet far more than expected.

This led to Kaynes’ net working capital cycle increasing from 87 days in FY25 to 125 days in FY26, with receivable days alone rising to nearly 134 days. As a result, the company reported negative operating cash flow during the year despite maintaining strong revenue growth. In a business where margins are relatively thin, a sharp rise in receivables can quickly start weighing heavily on cash flows and investor confidence.

While the company continues to make strides on various fronts including OSAT facility in Sanand, which remains an important step towards diversification and moving up the semiconductor value chain, the sharp increase in working capital blockage has become a major concern for investors.

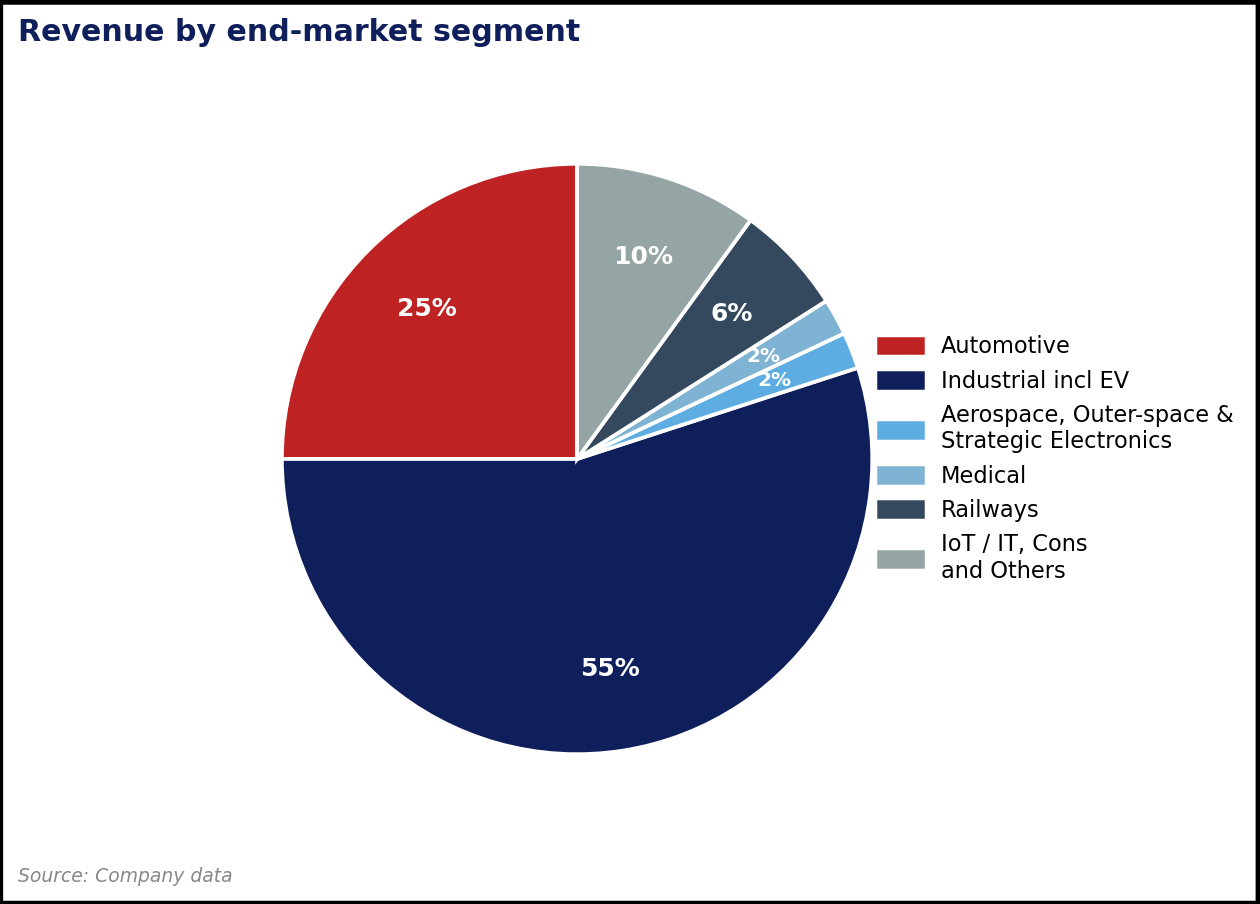

Amber Enterprises – Scale Through Diversification

Unlike Dixon and Kaynes, where recent pressures have emerged from product concentration and customer-related stress respectively, Amber appears relatively better positioned because of its diversified business mix and presence across multiple end markets.

Amber started as India’s leading Room Air Conditioner (RAC) OEM/ODM player, with nearly 72% of revenue coming from RACs and related components at the time of its 2018 IPO. Since then, the company has diversified significantly through backward integration into components like heat exchangers, motors, and PCBs, while also expanding into washing machines, commercial HVAC, and newer AC categories. RAC finished units now contribute around 43% of consolidated revenue.

Electronics has now emerged as Amber’s biggest growth driver. Through subsidiaries like ILJIN Electronics and acquisitions such as Ascent Circuits, Power-One Microsystems, and Unitronics, the company has built capabilities across PCB assembly, power electronics, EV chargers, solar inverters, battery storage, and industrial automation. Management expects electronics to contribute 30-40% of revenue over the next three years.

Alongside this, Amber has also built a meaningful railways and defence business through Sidwal. What began as a railway HVAC business has expanded into train doors, gangways, and defence cooling systems, with the segment now carrying an order book of over ₹2,600 crore, against FY26 revenue of roughly ₹450 Cr.

Despite the diversification, Amber is not completely insulated from the broader pressures impacting the EMS and consumer durables ecosystem. In Q4FY26, margins in the consumer durables division contracted by nearly 90 basis points YoY to 7.5%, impacted by rising raw material costs and currency depreciation. The PCB business also faced pressure as copper-clad laminate (CCL) and gold prices surged nearly 60% over the last year.

Since Amber operates as a Tier-2 supplier in several segments, there is typically a lag of one to one-and-a-half quarters before higher input costs can be passed on to customers, leading to temporary margin pressure.

Simlar to Kaynes, they also saw working capital cycle stretch after management deliberately increased inventory to safeguard against geopolitical and supply chain disruptions. Net working capital days increased from 9 days in March 2025 to 29 days by March 2026.

Overall, the current slowdown in India’s EMS sector appears less like a structural breakdown and more like a phase where company-specific execution and business mix differences are becoming far more important. Dixon is facing product concentration risks due to its heavy dependence on smartphones, Kaynes is dealing with customer and receivable-related stress in smart metering, while Amber appears relatively better placed because of its diversified presence across RACs, electronics, railways, defence, and industrial segments.

Despite the near-term slowdown, the long-term opportunity for India’s EMS and electronics manufacturing ecosystem remains largely intact for three key reasons.

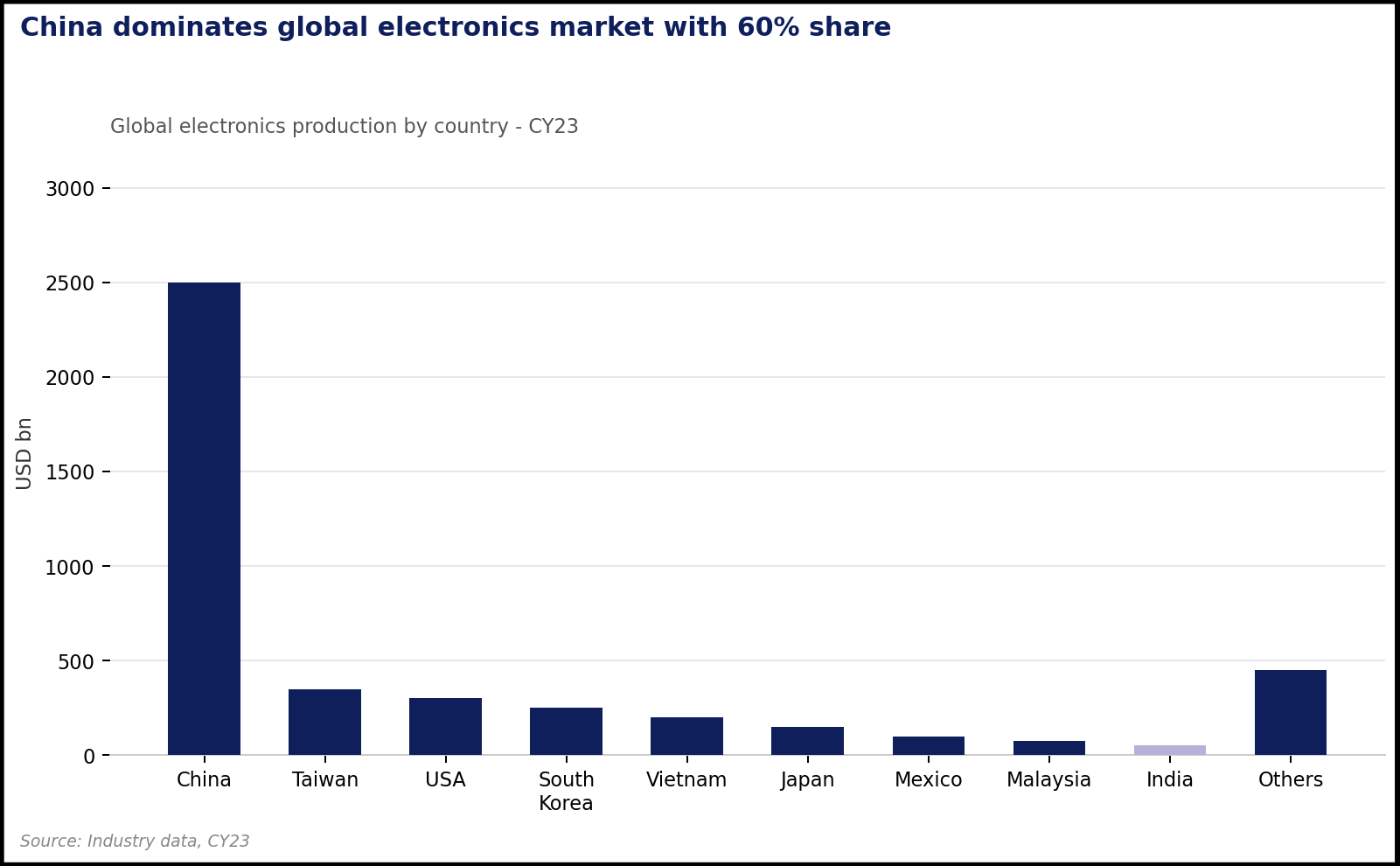

- India still remains a very small player in the global electronics manufacturing landscape. China alone accounts for nearly 60% of global electronics production, while India’s share remains tiny despite the significant growth seen since 2014. This suggests that even a modest shift in global supply chains away from China could continue to create a disproportionately large opportunity for Indian manufacturers over the next decade.

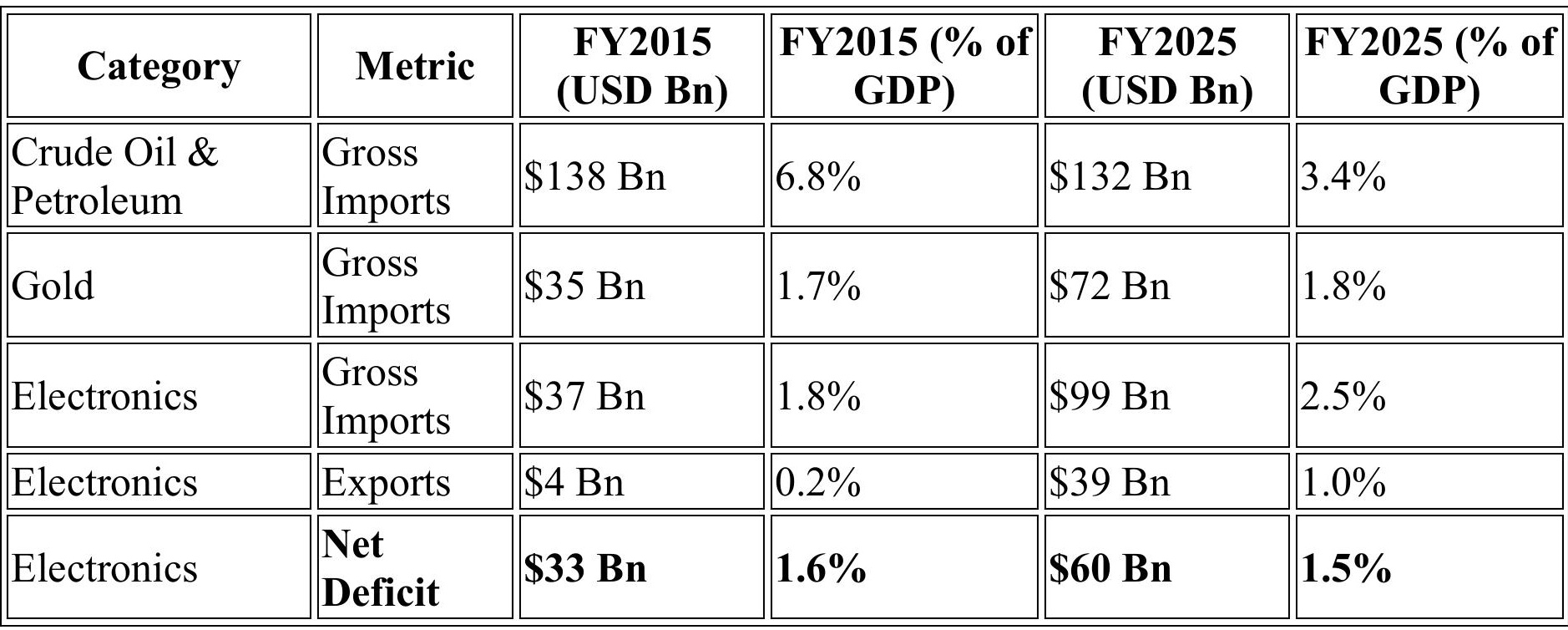

- India continues to remain heavily dependent on electronics imports. Electronics imports have risen from roughly $37 Bn in FY15 to nearly $99 Bn in FY25, making electronics one of India’s largest import categories after crude oil. Even after a decade of manufacturing push, the country still runs a net electronics trade deficit of nearly $60 Bn annually. This itself highlights the large domestic substitution opportunity that still exists ahead for component makers, EMS companies, semiconductors, PCBs, displays, and other electronics value chain players.

- Government policy support remains firmly intact and is in fact expanding into deeper parts of the electronics value chain. While some earlier mobile-focused PLI schemes are nearing expiry, the government has simultaneously launched newer initiatives like the Electronics Components Manufacturing Scheme (ECMS), expanded semiconductor incentives under India Semiconductor Mission (ISM), and increased support for ATMP/OSAT, display fabs, and component manufacturing. The Union Budget 2026 increased ECMS outlay to ₹40,000 Cr while ISM 2.0 is now focused on backward integration, semiconductor equipment, materials, and domestic chip design capabilities.

While the sector may be entering a tougher phase after years of hyper growth, the broader India electronics manufacturing story remains far from over. Near-term challenges around margins, working capital, and slowing demand are largely exposing company-specific weaknesses rather than signalling the end of the opportunity itself.

Perhaps the bigger question is not whether EMS is going out of favour, but whether the sector is simply moving from a phase of easy growth to one where execution quality matters far more.