Mapping the Path to Higher Value Addition

In 2014, India made barely one in four mobile phones it consumed. Everything else arrived in a box, fully assembled, mostly from China. A decade later, the story has inverted almost completely.

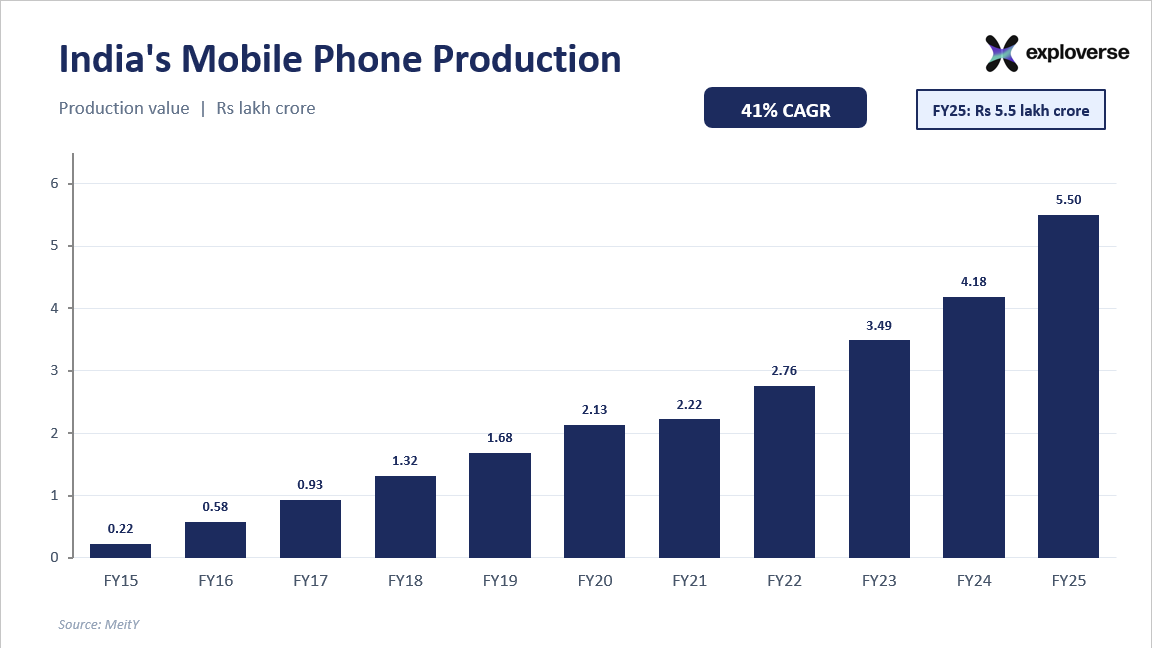

Domestic production has climbed from 26% in 2014 to 99.2% today, with mobile exports surging from just Rs 1,566 crore in FY2014-15 to Rs 1.2 lakh crore in FY2023-24. India manufactured 212 million mobile phone units in 2024, cementing its place as the world's second-largest producer. And in a milestone that few would have predicted even five years ago, smartphones became India's single largest export commodity in 2025, overtaking fuel and diamonds.

Overall electronic goods production has surged nearly six-fold, from Rs 1.9 lakh crore in 2014-15 to Rs 11.3 lakh crore in 2024-25 (about 50% being mobile phone alone), while exports have grown eight-fold over the same period. Apple's India pivot alone tells a significant part of the story: iPhone suppliers collectively manufactured devices worth $14 billion in India during FY24, representing 14% of Apple's global output, with a stated ambition to source the majority of US-bound iPhones from India by end of 2026.

But here is where the honest version of this story gets interesting. Almost all of this growth is assembly. The chips, the display, the camera sensors, the modem - the components that account for 80 cents of every dollar of a phone's value - still arrive in India from Taiwan, South Korea, Japan, and China. India screws the device together, tests it, boxes it, and ships it which has created hundreds of thousands of jobs & built industrial capacity. But it is the first chapter, not the whole book.

How It Happened?

India's mobile manufacturing surge was the product of a specific policy architecture, a geopolitical tailwind, & a sequence of government decisions that, for once, arrived in roughly the right order.

First came the ‘Make in India’ initiative launched in 2014 was accompanied by a phased manufacturing programme that steadily raised import duties on finished mobile phones while keeping duties on components lower. Intent was to make it expensive to import a finished phone, and manufacturers find it cheaper to assemble in India. The number of mobile phone manufacturing (mostly assembly stage) units jumped from just two in 2014-15 to over 300 by 2024-25.

Then came the ‘Production Linked Incentive (PLI)’ scheme, launched in April 2020, was the second and more sophisticated lever. Rather than simply taxing imports, PLI paid manufacturers a % of incremental sales above a baseline, rewarding scale and targeting global champions directly. Apple's contract manufacturers, Foxconn, Pegatron, and Wistron (now Tata Electronics), all qualified. So did Samsung. The PLI scheme for mobile manufacturing attracted Rs 17,519 Cr in investment, more than double its original target, with production exceeding goals by 36% at Rs 8.12 Lakh Cr. Smartphone exports reached Rs 2.62 Lakh Cr in 2025.

Further, measures like lowering basic customs duty on PCBs, and chargers from 20% to 15% in Union Budget 2024-25, while also exempting critical minerals and inputs required for smartphone manufacturing. Intent of the government throughout was to was willing to reduce the cost of inputs to keep India competitive as an export base, not just a protected domestic market.

Hard Truth

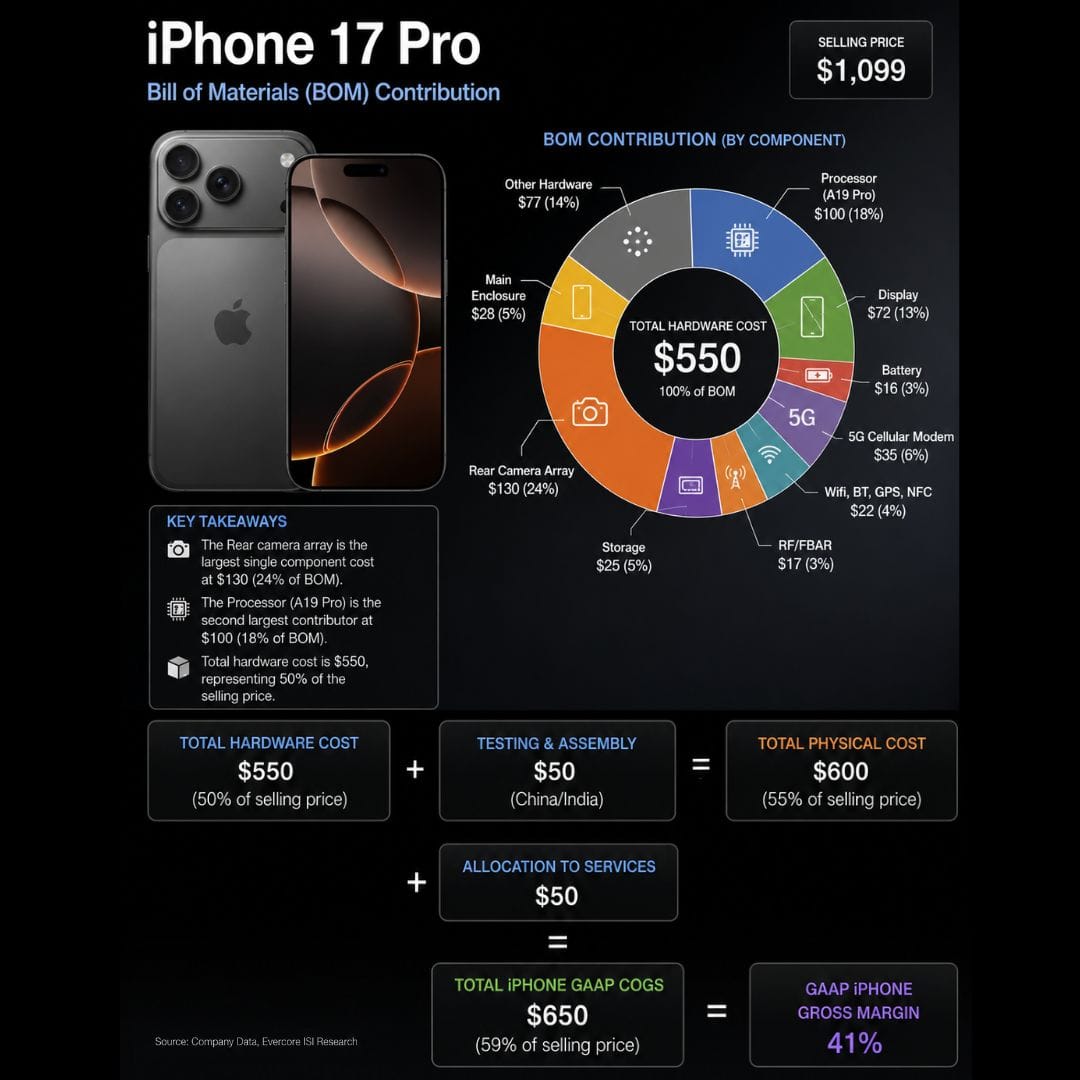

India is now the world's second-largest mobile phone manufacturer. But it is capturing less than 8 cents of every dollar of value in the phones it makes. Of the $600 it costs to physically produce an iPhone 17 Max assembled in India, $500 worth of components generally arrive at the factory gate already made, already valued, already profitable for someone else:

- Taiwan captures the processor margin.

- South Korea captures the display margin.

- Japan captures the camera margin.

Whereas, India captures the labour and overhead on the final step: putting it all together.

At the volumes India now operates, that $50 per unit translates to hundreds of thousands of jobs & industrial capability.

This is what economists call the ‘Smile Curve’ problem. In any global value chain, the two ends, design and branding on one side and after-sales and services on the other, capture the most value. The middle, physical manufacturing and assembly, captures the least. India has entered the value chain precisely at its least lucrative point.

The iPhone 17 Pro sells for $1,099. Its GAAP cost of goods is $650. Apple’s gross margin is 41%. Of that $650 in costs, India contributes $50, or roughly 7.7%. The problem is that India is booking the revenue on its export ledger at the full factory-gate value of the phone, while capturing only a small fraction of the actual value created.

When a Tata Electronics or Foxconn India facility imports aluminium ingots and runs them through CNC machining lines to produce a chassis, the labour, electricity, tooling amortisation, and factory overhead on that machining operation all count as Indian value addition. While the ingot/cells arrived from abroad, the finished batterychassis is ‘Made in India’. Every rupee spent turning one into the other goes into the numerator which therefore shows India’s value addition is ~15 to 20%.

Though, iPhone example is a ceiling case. The iPhone 17 Pro represents the most import-intensive smartphone on the planet:

- A19 Pro processor is fabbed at TSMC on a 3nm node.

- Display is a custom LTPO OLED from Samsung Display.

- Camera array uses Sony’s most advanced stacked CMOS sensors.

There is almost nothing in that bill of materials that any country other than Taiwan, South Korea, or Japan can currently make at the required specification.

Move down the product ladder and the picture changes considerably. A Samsung Galaxy A-series mid-ranger assembled in Noida has a materially different component mix. The processor is a less exotic node. The display is an AMOLED panel but sourced from Samsung’s own captive supply, with some mid-range panels now coming out of BOE’s China lines at lower cost and simpler specs. Plastic rear covers, charging ICs, and structural components are increasingly sourced domestically. India’s DVA on a mid-range Android likely sits 4 to 6% points higher than on a flagship iPhone, on a comparable denominator basis.

Go further down to a domestically-branded device, a Micromax, Lava, or Karbonn handset targeting the sub-Rs 8,000 segment, and the gap widens further. These phones use MediaTek chipsets fabbed offshore but rely heavily on domestic injection moulding, domestic PCB assembly, and local battery pack integration. The display is a basic LCD panel, still imported, but simpler and cheaper. Domestic value addition on these devices can approach 20 to 25% even on a rigorous GVC basis, not just the narrow PLI denominator.

What India Can Win & When

Some analysis on key components:

- Mechanical Sub-Assemblies: Already HappeningFew mobile components like SIM trays, CNC-machined chassis, injection-moulded housings, and structural brackets are already substantially domestic today. This is India’s head start from PLI and the next step is now engineering plastics, moving from commodity polymers into high-performance materials like PEEK and LCP used in antenna windows and connector housings and is actionable immediately under ECMS capex incentives.

- PCBs and Copper Clad LaminatesCompanies like Kaynes Circuits is committing 87% of its Rs 3,280 crore ECMS investment to PCBs and laminates, targeting full domestic demand coverage for polypropylene film and copper laminates. Standard multilayer boards are winnable within 3 to 5 years. HDI boards, used in flagship smartphones, require laser drilling and precision etching at micron tolerances & are a longer project.

- Battery CellsPack assembly is domestic but the gap is in the cell, and beneath that, the cathode active material. NMC and LFP cathode powders come almost entirely from China and South Korea. The ACC-PLI was announced in 2022 but could not achieve its desired objectives. India risks assembling cells from imported chemistry, the same trap as PCB assembly without CCL and hence the fix requires policy coordination.

- Camera Modules: Assembly StartedModule assembly has begun at Foxconn and Tata facilities. The value, however, sits in the lens barrel, the image sensor, and the voice coil motor actuator, none of which India currently makes. The lens barrel is the most accessible as precision plastic injection moulding for aspheric lenses is not semiconductor-class manufacturing. A focused optical cluster in Hyderabad or Pune, building on existing defence precision manufacturing, could localise lens production within five years.

- Semiconductors: The 2030s ChapterSemiconductors are 25 to 30% of smartphone BoM. India’s domestic contribution is zero. Flagship processors are fabbed at TSMC at 3nm. Tata-PSMC in Dholera targets 28nm to 65nm, serving automotive and industrial markets, not smartphone-grade logic. Micron’s Sanand plant does packaging, not wafer fabrication. Display driver ICs, PMICs, and audio codecs are all imported with no domestic IP in the stack.

The investments are right but the timeline is honest: this is a 2030s story. But the good news is that the base is setting up well.

To Conclude

The smartphone BoM shows exactly where the gaps remain. Mechanical parts, PCBs, and battery components are within reach. Displays, camera sensors, and semiconductors are not. The objective should not be to localise everything, but to systematically move into the components that capture the most value.

A decade ago, India imported the phone. Today, it assembles the phone. The next decade will determine whether it can build the components that matter and capture a larger share of the economics.