Can India break free from PCB import dependence?

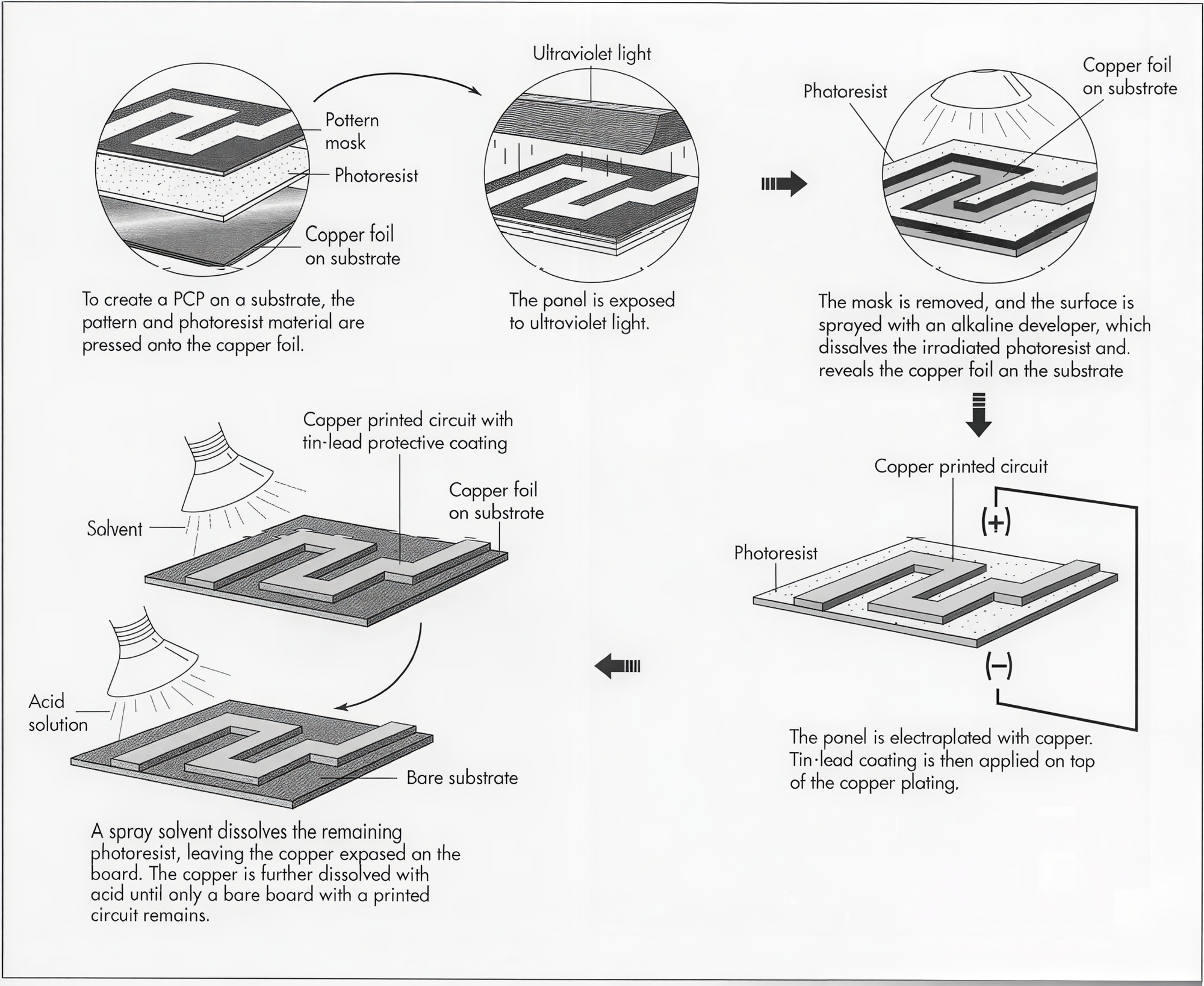

Every smartphone, laptop, television, automobile, defence system, or industrial machine runs on a hidden foundation most consumers never notice: the printed circuit board, or PCB. Often called the ‘backbone’ of electronics, a PCB is the platform that connects and powers all electronic components inside a device and helps semiconductors, sensors, memory chips, and processors communicate with each other.

")

Yet despite India emerging as a major electronics assembly hub, the country remains heavily dependent on imports for PCBs, especially advanced multilayer boards used in smartphones, servers, telecom equipment, and automobiles. Much of this supply today comes from countries like China, Taiwan, South Korea, and Vietnam. This creates a major gap in India’s electronics manufacturing ambitions, where final products may increasingly be assembled locally, but a large share of the core electronic backbone is still imported. And the day that exporting nation decides to use this dependence as a strategic lever, whether through export restrictions, trade disputes, or supply disruptions, India’s electronics value chain could face significant vulnerabilities. Building domestic PCB manufacturing capabilities is therefore not just an economic opportunity, but increasingly a matter of supply chain resilience and strategic autonomy.

What makes this more interesting is that India was not always so dependent. In the 1980s, the country had a growing domestic PCB manufacturing ecosystem supported by government policies, public sector demand, and an early push toward electronics self-reliance. So how did India move from having indigenous PCB manufacturing capabilities to becoming deeply import dependent today? In today’s blog, we will trace this journey and understand the key policy decisions, global shifts, and missed opportunities that shaped India’s PCB industry over the last four decades.

How it Started?

Bharat Electronics Limited established its PCB manufacturing facility as early as 1968, and throughout the 1980s it served the bulk of defence, radar, and government electronics demand with captive in-house production. ITI (Indian Telephone Industries) and ECIL similarly fabricated boards for their own verticals: the telephone exchanges, the CDOT digital switches, the Doordarshan transmitter rollout.

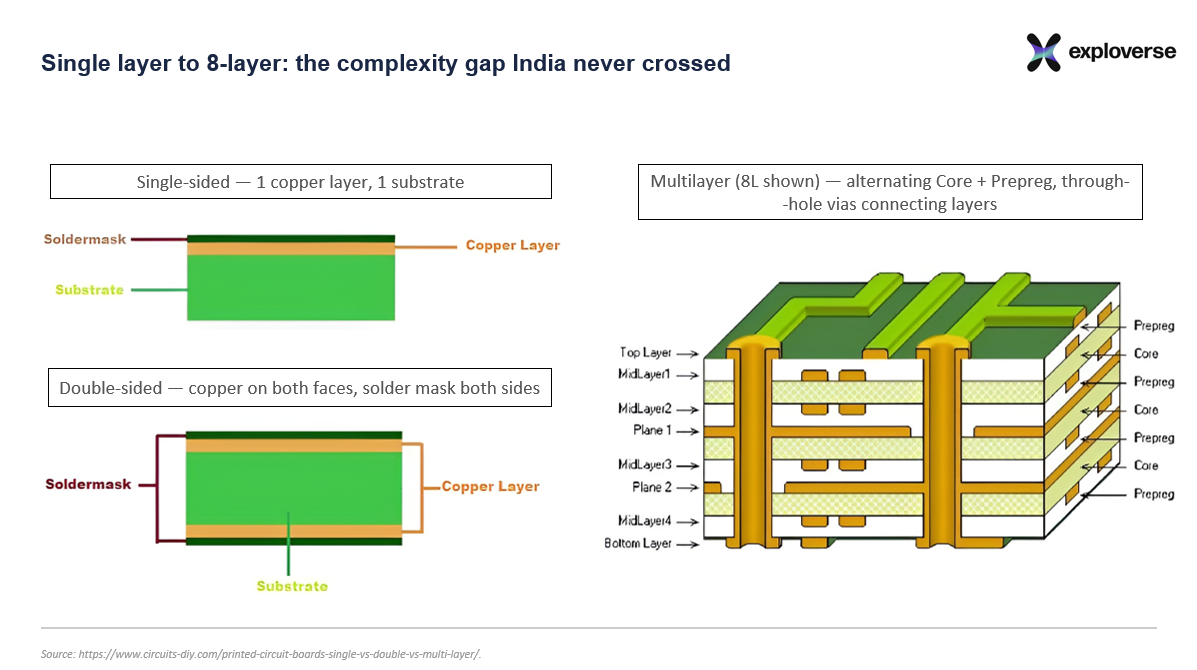

By the late 1980s, Sulakshana Circuits (1988), Garg Electronics (1989), and a wave of small-scale units seeded by the government's MTB scheme had joined them, collectively covering single-sided and double-sided board requirements for the booming TV assembly and early PC manufacturing sectors.

While domestic manufacturers were already capable of producing double-sided PCBs locally, they still depended on imports for key raw materials such as copper-coated glass epoxy sheets, as India lacked domestic production of sheets with the required 17.5-micron copper thickness. This implied India’s PCB dependency was concentrated more on the upstream side of the value chain.

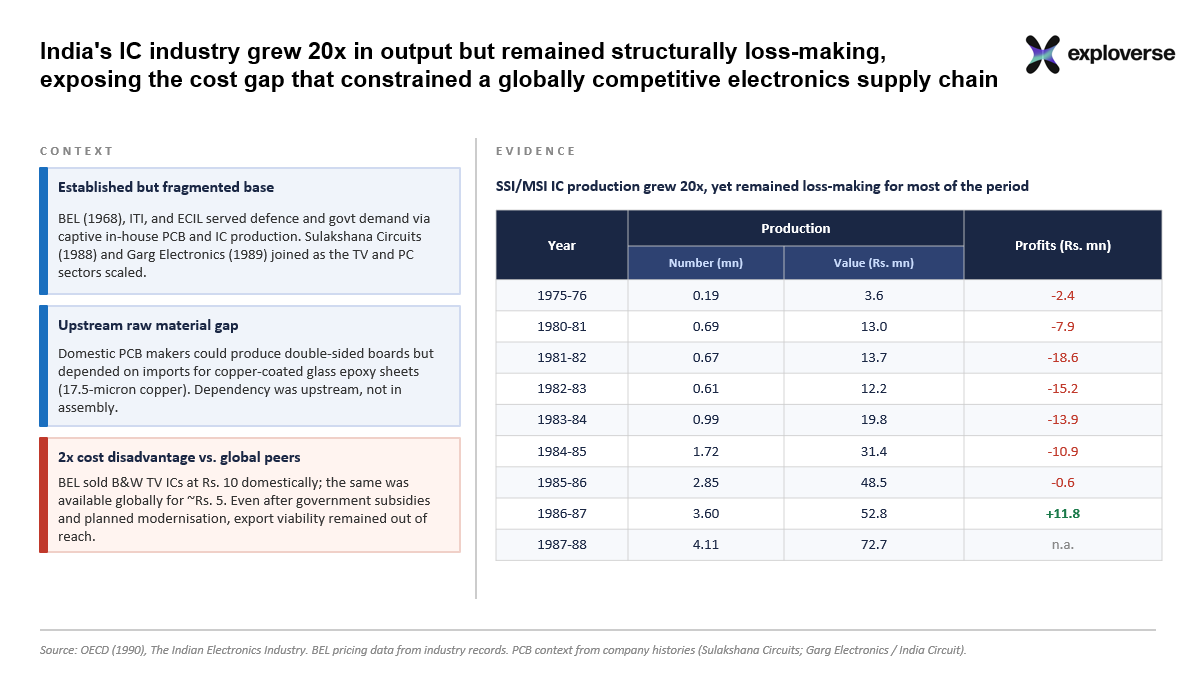

However, India’s challenges in electronics manufacturing extended beyond raw material dependence. Even in segments where domestic production capabilities existed, manufacturers often struggled to achieve globally competitive economics. A case in point was the country’s early integrated circuit (IC) industry. As shown in the table below, production of SSI/MSI integrated circuits increased more than twenty-fold between FY1976 and FY1988, rising from 0.19 million units to over 4.1 Mn units. Yet for most of this period, the industry remained loss-making despite the growth in output.

BEL sold its ICs for B&W TVs for Rs. 10 in India, while internationally they are available for about Rs. 5. Even when all government incentives and subsidies are taken into account, and their plant’s modernization realized, the export market will still not be profitable. (source)

Together, these constraints prevented India from building a globally competitive electronics supply chain despite having established capabilities across several parts of the value chain.

Rising Complexity, Rising Dependence

By the 2000s, that equation had quietly but completely reversed. India was no longer importing raw materials to manufacture PCBs locally. Instead, it had begun importing finished boards, and increasingly, fully assembled printed circuit board assemblies (PCBAs) with all components already mounted on them. The reason was simple: India's rapidly modernising economy had become far more sophisticated than what its surviving PCB manufacturers were capable of producing.

The shift was triggered by the explosion of new electronics categories through the 1990s and 2000s. India’s first mobile phone call was made on July 31, 1995, and companies like Nokia, Motorola, and Ericsson soon entered the market. Alongside mobile phones came personal computers, telecom switching equipment, cable set-top boxes, and other electronic devices that required significantly more advanced circuit boards than the single-sided and double-sided PCBs commonly produced in India during the 1980s.

A mid-1990s feature phone typically required a 4-to-6-layer PCB with fine-pitch surface mount components. Desktop computer motherboards evolved toward 6-to-8-layer boards with controlled impedance routing.

By the 2000s, even a Nokia handset required sophisticated boards featuring blind and buried vias, technologies that demanded laser drilling and advanced fabrication capabilities unavailable in India. As component density increased and chip packaging became more compact, the industry rapidly transitioned towards multilayer PCBs capable of stacking multiple interconnected circuits within a single board. India, having never meaningfully invested in this next generation of fabrication capabilities, found itself increasingly unable to keep pace with global technological requirements.

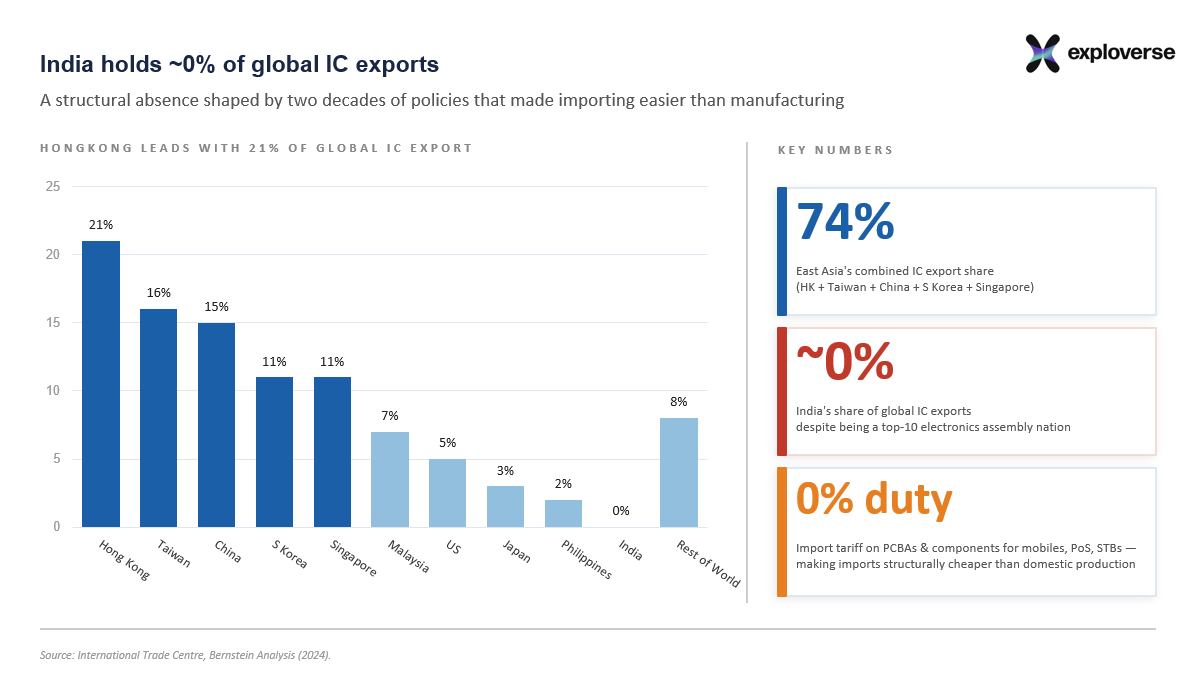

So, instead of building domestic fabrication capacity, Indian assemblers and global electronics brands found it easier and significantly cheaper to import finished PCBAs directly from countries such as China, Taiwan, South Korea, and later Vietnam. Government policies unintentionally accelerated this shift.

Zero-duty imports on components and sub-assemblies for high-growth products like mobile phones, PoS machines, micro-ATMs, and set-top boxes reduced the incentive to manufacture components locally.Duty-free imports of PCBAs directly weakened demand for domestically manufactured PCBs and discouraged fresh investment into the segment.

In an effort to make electronics more affordable and scale assembly-led manufacturing, India created an ecosystem where importing a completed board from East Asia was structurally cheaper and easier than building the deep manufacturing infrastructure required to produce one domestically.

India’s PCB industry largely remained stuck at the single-sided and double-sided board stage, while the rest of the world moved rapidly towards advanced multilayer, high-density, and precision-engineered PCBs required for modern electronics. As a result, when products like the iPhone are manufactured in India today, there is often little choice but to import the sophisticated PCBAs and critical electronic sub-assemblies from global supply chains dominated by East Asia.

More Devices, More Boards: Why Electronics Dependence Only Deepens

To understand why India’s PCB import problem is structurally worsening rather than simply persisting, one must first reckon with how completely electronics have colonised daily Indian life over the past three decades. In 1990, a typical Indian household might have owned a television, a transistor radio, and perhaps a landline telephone. That was largely the extent of it. Electronics was a category most Indians encountered, not one they lived inside.

Today, the same household is likely to own multiple smartphones, a flat-screen television, a washing machine with a digital control board, an inverter air conditioner, a WiFi router, and a two-wheeler or car whose engine management system, ABS, and instrument cluster are all electronically governed. Each of these products contains at least one PCB. Many contain several.

The average middle-class Indian household in 2024 likely carries more circuit board area within its walls than an entire small factory floor would have in 1985.

In 1999, just 7% of Indian households owned a landline phone; by 2005, that figure had peaked at 14%. Today, less than 1% of homes have a landline phone, but mobile phone ownership has exploded, democratising telephony in a way landlines never could. In 2008, India had 346 million registered mobile SIM cards; between 2008 and 2024, that number more than tripled. Every one of those handsets, whether a feature phone or a smartphone, carries a PCB inside it. The shift from feature phones to smartphones alone multiplied PCB complexity per device by an order of magnitude: a flagship smartphone PCB today can have 12 to 16 layers, compared with the 4 to 6 layers of a mid-2000s Nokia handset. More users, and more circuit board content per user: both variables have moved simultaneously and sharply upward.

A Maruti 800 of the 1990s had a carburettor, a simple ignition system, and almost no electronic governance, perhaps one or two rudimentary control modules. A mid-segment passenger car sold in India today is a fundamentally different machine. Modern cars incorporate between 30 and 100 Electronic Control Units (ECUs) that manage powertrain, infotainment, safety, and autonomous driving functions, and each ECU is anchored by a PCB. EVs require an average of 95 ECUs per vehicle, compared with around 70 in traditional internal combustion engine vehicles, as battery management, thermal regulation, and power conversion introduce entirely new electronic systems.

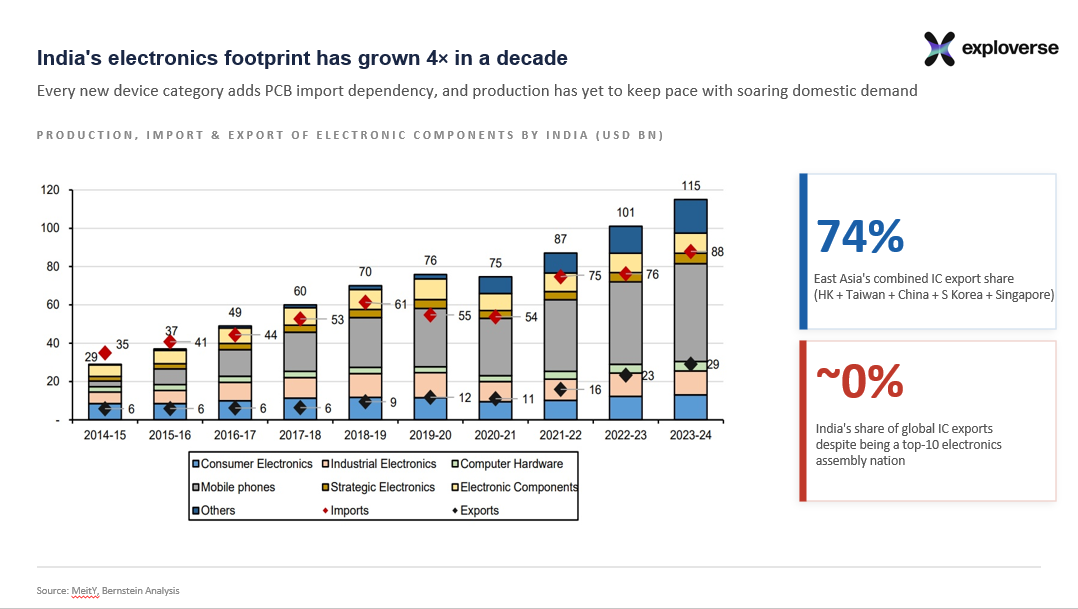

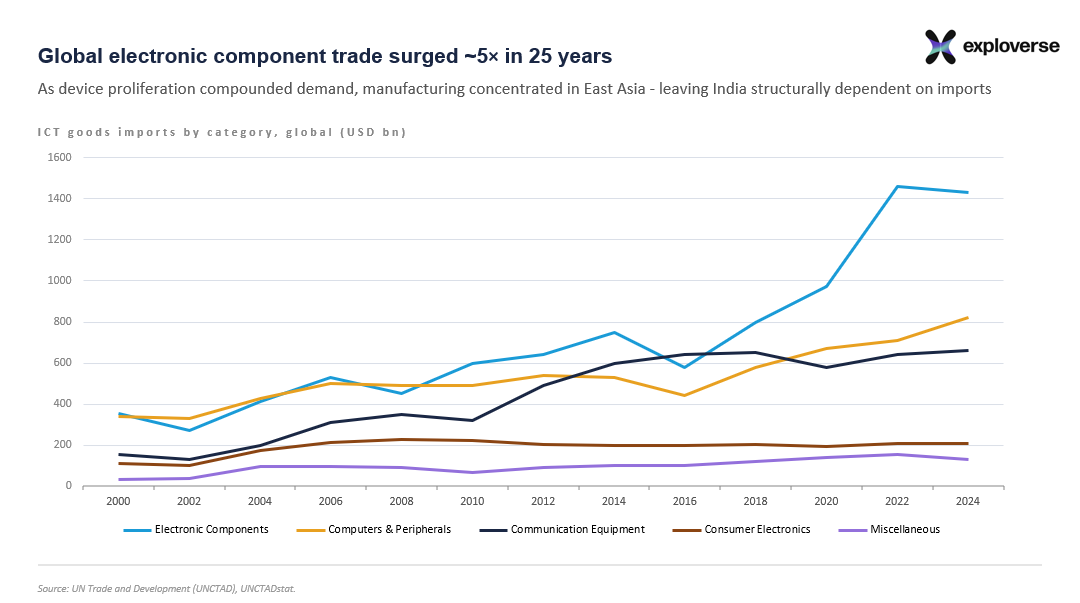

Therefore, global trade in electronic components, including chips, circuit boards, and sensors, has surged nearly fivefold over the last 25 years. At the same time, manufacturing has become increasingly concentrated in a handful of countries, leaving much of the world, including India, dependent on imports for these critical components.

Breaking the Dependency: What India's PCB Policy Must Get Right

India's PCB dependence is not the result of a single policy mistake, nor can it be solved through a single subsidy scheme. The industry's weakness today reflects decades of underinvestment across the entire value chain, from raw materials and fabrication technology to ecosystem development and skilled manpower. If India is serious about building a globally competitive PCB industry, the policy response must address the structural bottlenecks that have prevented domestic manufacturing from scaling in the first place.

Five areas, in particular, stand out.

- Use Government Procurement to Create Demand. India's defence sector, railways, public-sector telecom infrastructure, and government electronics programmes collectively consume billions of dollars worth of PCBs every year. A clear policy requiring that government-procured electronics above a certain threshold value incorporate domestically manufactured PCBs, with a defined phase-in schedule, would create the anchor demand that Indian fabs need to justify large-scale capital investment. Building an HDI PCB facility requires significant upfront capital and a multi-year payback period. Without predictable long-term orders, few private investors will be willing to commit capital to such projects. Government procurement can therefore play a critical role in creating the initial scale required for the industry to become commercially viable.

- Building Clusters is Key: A PCB factory without a surrounding ecosystem is not a competitive PCB factory. It is an import-dependent assembly point with extra steps. What made Shenzhen and the Pearl River Delta the world's PCB centre was not a single factory, but the co-location of CCL suppliers, chemical vendors, equipment maintenance companies, laser-drilling specialists, trained process engineers, logistics infrastructure, and environmental treatment facilities, all within a radius where proximity reduces costs and turnaround times.

- Build the Talent Pipeline: India's PCB industry suffers from a severe talent gap at almost every level: PCB design engineers who understand HDI and high-frequency board constraints, process engineers who can manage sequential lamination and laser-via drilling, quality professionals certified to IPC-6012 and IPC-A-600, and chemists who understand the plating-bath chemistry that separates a reliable board from a defective one. China attracted foreign capital and manufacturers, which brought both technology and talent, enabling the transfer of knowledge and expertise to the domestic ecosystem. India will have to adopt a similar approach, tailored to its own strengths and circumstances.

- Fix the Raw Material Bottleneck: About 90% of the copper-clad laminates (CCLs) and specialty chemicals used by India’s PCB industry are still imported, predominantly from China, Taiwan, and South Korea. This dependence on imported CCLs, the single most important input in PCB manufacturing, remains the industry’s biggest structural disadvantage. The result is a cost disadvantage that exists before a single board is produced. No amount of downstream manufacturing incentives can fully bridge this gap without first addressing the upstream input layer.

A Chinese PCB manufacturer sources laminates domestically at scale, benefiting from lower costs, shorter lead times, and a tightly integrated supply chain. An Indian manufacturer often buys the same material from the same origin, but at a premium, with longer lead times and additional currency risk.

- Develop a Domestic Capital Goods & Advanced Materials Ecosystem: Critical machinery used in PCB fabrication is predominantly imported, particularly from China, while key components such as precision drills, plating chemicals, and manufacturing consumables continue to be sourced externally. These dependencies increase costs, elongate supply chains, and expose the industry to geopolitical and trade-related disruptions. Building domestic capabilities across equipment manufacturing, specialty chemicals, consumables, and process technologies will be essential to creating a resilient and globally competitive PCB ecosystem.

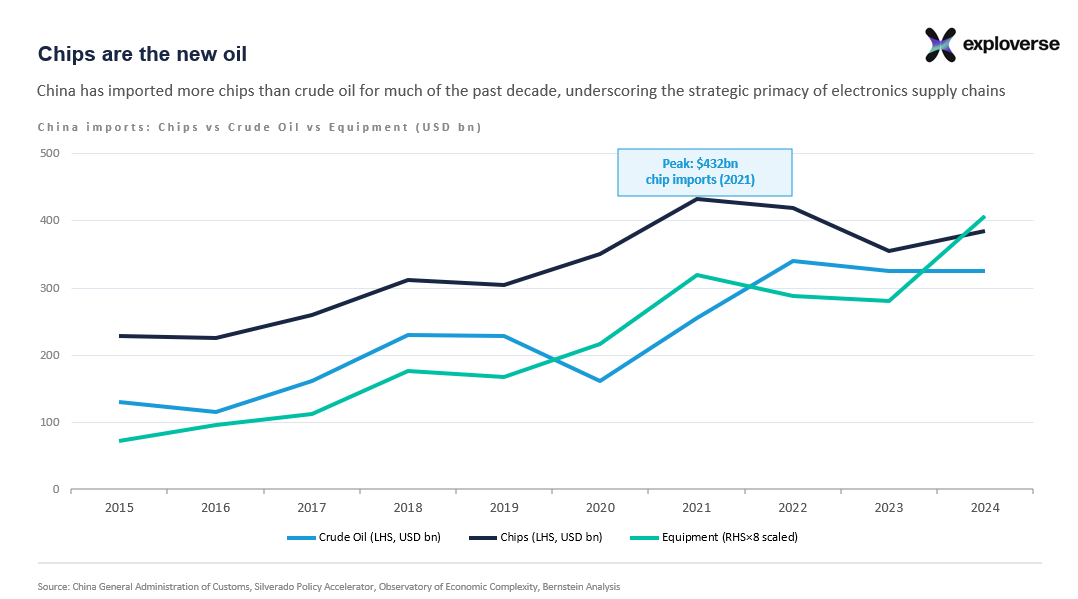

New Oil of the Digital Economy

If oil powered the industrial economy of the 20th century, chips and electronic components are powering the digital economy of the 21st. As the chart shows, China has spent more on importing chips than crude oil for much of the past decade, showcasing the growing strategic importance of electronics supply chains.

The broader lesson from every country that successfully built a PCB industry, whether Taiwan, South Korea, Japan, or, eventually, China, is that the journey took fifteen to twenty years of sustained, sequenced, and occasionally uncomfortable policy commitment. A strategic joint-venture framework, coupled with a clear ten-year PCB Vision Roadmap, can accelerate India’s integration into the global value chain, but only if that roadmap is treated as a binding national industrial commitment rather than a ministry presentation.

India assembled its way to becoming the world’s second-largest smartphone manufacturer without making a single PCB for those phones. The next chapter requires doing what is actually harder: building the manufacturing foundation that makes final assembly truly meaningful.